Since the courts have punted AOB reform to lawmakers, we now know who, and to some extent how, to give consumers needed reforms. That doesn’t mean that the executive branch isn’t needed to assist. Indeed…it doesn’t mean that its’ inaction or decision making, so far, isn’t partially responsible for the continuing consumer abuse.

It simply means that those of us who care need to pull out all stops to get the job done. I’ve been talking to industry, business and consumer groups (FAIR, United Policyholders, et al) telling them to get involved up to their eyeballs. Some are involved. Others soon will be.

Policymakers can no longer play the blame game; and, won’t if we don’t let them. Florida’s cabinet must put pressure on lawmakers, particularly the leadership, to finish the job they barely started last session. And we must all put pressure on lawmakers by holding them accountable for any further inaction on this most important problem.

The Florida Chamber of Commerce is stepping up! It’s recent piece will help those in the insurance industry provide a “non-insurance” point of view to policyholders. Agents, in particular, can use the following as a mailer for their clients and as a handout for local civic groups or to accompany luncheon presentations.

Here, with permission, is the Chamber’s cogent piece showing the need for AOB reform. (Click graphs to enlarge).

____________________________________________

Florida Chamber Exclusive Property Insurance Update

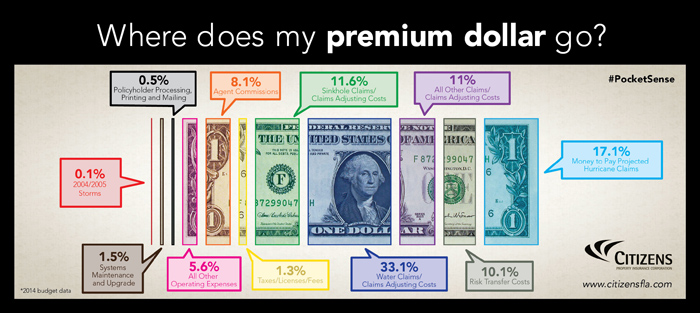

Citizens Property Insurance, the state run property insurer, recently released how every premium dollar is spent. More than half of every premium dollar in 2014 was used to pay non-hurricane claims and adjustment costs, and nearly one-third of every premium dollar was spent on water claims alone. This means more than half of every premium dollar policy holders pay is going toward non-hurricane claims, and a portion of this money is being spent on inflated claims because benefits are assigned over to a third party and repairs are made without the insurer’s knowledge.

(click to enlarge)

Inflated claims through assignment of benefits are not a unique issue to Citizens Property Insurance and have been prevalent among all insurers. This is the result of an increase in the number of claims in which the policy has been signed over to a third-party repairing the damage, where the third-party is also working with a trial lawyer. In these instances, the damages are repaired before the insurer can even come out to adjust the claim, and then the trial lawyer sues for additional damages beyond what was necessary. The “assignment of benefits” issue is one the Florida Chamber has been actively fighting to reform in an effort to reduce fraud and abuse in our state’s insurance system. This issue is especially problematic in Miami-Dade County.

Inflated claims through assignment of benefits are not a unique issue to Citizens Property Insurance and have been prevalent among all insurers. This is the result of an increase in the number of claims in which the policy has been signed over to a third-party repairing the damage, where the third-party is also working with a trial lawyer. In these instances, the damages are repaired before the insurer can even come out to adjust the claim, and then the trial lawyer sues for additional damages beyond what was necessary. The “assignment of benefits” issue is one the Florida Chamber has been actively fighting to reform in an effort to reduce fraud and abuse in our state’s insurance system. This issue is especially problematic in Miami-Dade County.

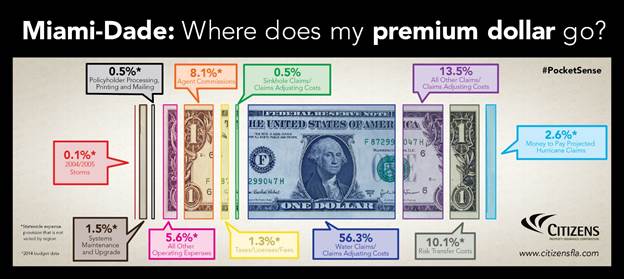

The statewide average for Citizens Property Insurance is 33.1 percent of every dollar of premium going to water claims and adjustment of these claims. But in Miami-Dade County, 56.3 percent of every dollar goes to paying out water claims. This also translates to the rest of the insurance market, which also pays out more in Miami-Dade than in any other Florida county for water claims.

(click to enlarge)

Although Florida has not had a hurricane in 10 years, the increase in the amount of non-catastrophic claims is driving up rates, especially with regard to water claims. The Florida Chamber is committed to reducing fraud while protecting homeowners from these unscrupulous practices.

Although Florida has not had a hurricane in 10 years, the increase in the amount of non-catastrophic claims is driving up rates, especially with regard to water claims. The Florida Chamber is committed to reducing fraud while protecting homeowners from these unscrupulous practices.

Share Your Experience:

Email Carolyn Johnson at cjohnson@flchamber.com to share your experience if you have been solicited by a contractor or repairman for property damage, or share the process you went through to get your repairs fixed by your insurance company.

##end##

IMPORTANT: If you enjoyed this post you’re invited to subscribe for automatic notifications by going to: www.johnsonstrategiesllc.com. Enter your email address where indicated. If you’re already on the website at Johnson Strategies, LLC, go to the home page and enter your email address on the right hand side. Remember, you’ll receive an email confirming your acceptance, so…check and clear your spam filter for notifications from Johnson Strategies, LLC. ENJOY

Mark Boardman says

Mark Boardman says

August 4, 2015 at 11:09 amScott

Could you expand on your thoughts on specific language you would use in proposed legislation. We seem to hear there is this problem. The lack of answers is the real issue. Ask your readers to also, provide specific language. Maybe someone will hit it just right for all parties.

Mark Boardman

scott says

scott says

August 4, 2015 at 12:37 pmMark, thanks for subscribing and for your question. Yes, wording and approach is the problem; politics and what is needed in the language to have buy-in from affected groups in order to maximize passage is the tough part. Putting that aside, we have some choices: 1) prohibit the use of AOB in property claims; 2) Insert language that allows carriers to have a prohibition against AOB in their forms (SFIC case), 3)my idea was to insert language requiring the use of a direction to pay for property losses, to help consumers. This would null the argument that the policyholder has to use their own funds. Other tributary needs are: 1) regulate water extraction business, 2) prohibit referral fees, plumbers, et al, 3)increase penalties for roofing fraud 4) reduce the public adjuster % from 20 to 12.5%. and more. I am willing, when asked, to develop language on any of these ideas and others. Hope my readers will come up with more. 🙂